Barring a pay raise, their high income won’t be enough for everything

For seven years, an Edmonton couple we’ll call Tina and Drake have lived by the gospel of their budget.

Neither one can point to exactly why they started laying out a budget or what influenced them to be so guarded with their money, but it has evolved into defining the couple’s way of life. Both Tina, 27, and Drake, 32, describe themselves as minimalists. Neither one of them really sees the point of spending money simply to own more things. As Drake puts it: “We don’t have a need to buy things and stuff we don’t want just to buy things and stuff.”

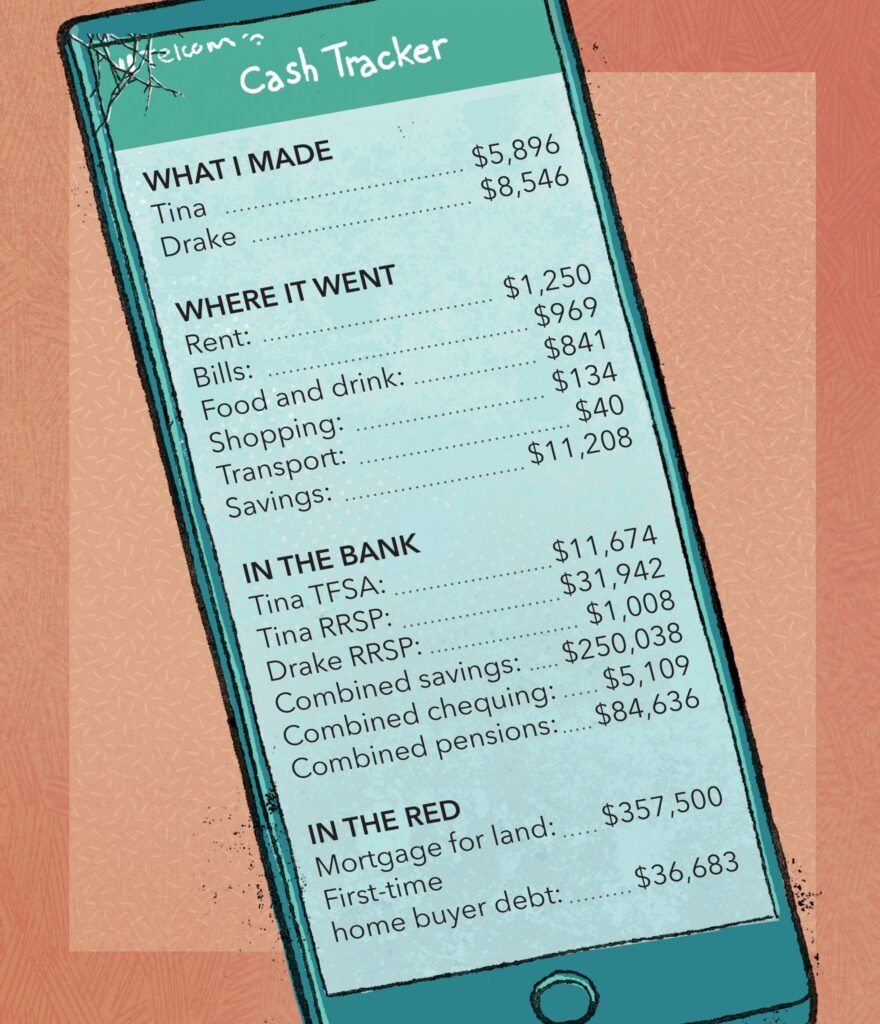

Combined, Tina and Drake, who both work in business consulting, earn more than $250,000 per year. Their budget is set up to allow them to save at least $10,000 of their monthly after-tax income of $14,442, or what amounts to 70 per cent of their income. There are many millennials who live rent-free at home with their parents that can’t even do that. But then again, most people enjoy buying things and stuff they don’t need just to buy things and stuff.

It’s their budget for discretionary spending that allows the couple to save so much. They only allow themselves $400 each in discretionary spending. Everything from buying a coffee to a new sweater is included in that allotment. If they spend that amount before the end of the month and a friend invites them out for drinks, they’ll decline to avoid going over budget.

Are you a millennial who wants to get the most out of your money? Contact Victor at vferreira@postmedia.com to appear in future edition of Spent, an entertaining look at the financial lives of real Canadian millennials.

Outside of the bills and groceries, their single-most expensive purchase was their Costco membership renewal at $63.

Even as they’ve moved from an apartment to buying a condo and earning multiple pay raises in between, they never once lost sight of this lifestyle. But now they’re worried that moving into their dream house and having a baby might change things.

“For us, it’s not really how do we cut expenses, it’s how do we maximize what we’re saving,” Tina said. “We want to know what’s the best way to approach this in the short-term without shooting ourselves in the foot for the long-term.”

Building a house from the ground up is both the most expensive and most exhausting project the couple has undertaken. Every cent of the $10,000 they save every month is going toward the downpayment. They’ve already paid $400,000 and will be making a second payment of $300,000 before they move in.

When it’s finished, the house will be worth $1.45 million. The main floor and second floor alone add up to 3,300 sq. ft, with three bedrooms and three bathrooms. The house also has an unfinished basement they could fill with an additional two bedrooms and another bathroom.

Tina and Drake only allow themselves $400 each in discretionary spending. Illustration by Brice Hall/National Post

They expect to finish the house in January, but until then there are going to be a few unknowns. The mortgage is one — Tina and Drake estimate it’ll be somewhere between $3,000 and $3,500 when all is said and done. Heating and electricity, for a house of this size, are expenses they’re unsure of. Then there’s the couple’s goal of having a child in the next two years.

Drake is used to having all the numbers in front of him so that he can plug them in and adjust his spreadsheets accordingly. Not having exact numbers is making him anxious. Tina is too. They don’t know how much they’ll be able to put away each month and whether it’ll still be enough to build their savings back up, bulk up retirement funds, take six-week vacations and afford a child.

I asked Raymond James financial advisor Janis Parmar for some perspective.

Tina and Drake are fortunate enough to generate a high income, but barring a pay raise, it won’t be enough for everything, Parmar said.

Let’s start with the house: Parmar put $3,500 of the couple’s monthly income towards paying the mortgage, assuming that it’ll come in higher than expected. The gas and electricity bill, for a house of that size, will also be pricey and could hit $1,500, Parmar thinks. Drake might disagree with this, but the couple’s discretionary spending will also have to be boosted, Parmar said, to accommodate for all the additional costs of moving into a new home. She’s giving each one an extra $300 to spend here.

“I think when they move in, they’re going to find that they’ve been being too strict,” Parmar said. “Tina is going to be walking past Bed, Bath and Beyond and say, ‘Oh boy, that’s a beautiful centrepiece that should go on my dining room table’ or ‘I have this chef’s kitchen so I should get these new pots.’ You cannot move from a one bedroom condo into a beautiful five bedroom home without spending money.”

You cannot move from a one bedroom condo into a beautiful five bedroom home without spending money

Janis Parmar, Raymond James financial advisor

Tina and Drake will also likely see their food budget increase, Parmar said, because they’ll want to host family and friends for dinner. (Drake joked the solution here would be a bring-your-own-hot-dogs BBQ). Cleaning bills might be another unexpected expense, Parmar said, because both Tina and Drake are working professionals and because after having washed the windows for a house that size once, Parmar suspects they’ll never want to do it again.

If the rest of the budget stays the same — $384 for groceries, $79 for auto insurance, $40 for gas, $96 for cable and internet and the remaining $12 on a phone bill that’s almost entirely covered by their employers — Tina and Drake would be able to save a maximum of $7,431.

Having a child will complicate things. Parmar said it could easily cost between $2,000 and $2,400 per month if we’re accounting for not just food, clothes, diapers and toys, but also child care, life insurance bills and RESP contributions.

A further decline to $5,000 per month still seems like it would leave the couple with more than enough, right? It is, until you factor in that Tina would be on maternity leave and would only be able to earn a maximum of $54,200. That means that the couple could quickly find themselves in a scenario where they only have between $1,000 and $2,000 to put away each month.

“It would be tight,” said Parmar who added that the couple would also have to do away with vacations, unless you count driving to Banff in a minivan. “They’re not going into debt, but they’re not going to have the big nest egg either.”

When I called Tina and Drake to relay the new budget, the first thing Drake did was pull up his spreadsheet on his laptop so he could follow along. I could tell some of the numbers hit him hard. He nervously laughed after double-checking that he could be spending a combined $3,900 per month on hydro and a child.

“That’s three times more than what I was expecting,” Drake said. “I still don’t know what the hell I would spend $3,000 on for a child.”

Drake also isn’t sure he needs the extra money in discretionary spending and admitted that he’d be tempted to cut it back down.

Even with far less at their disposal though, neither one is ready to do away their budget-based minimalist lifestyle.

“I’m confident in saying we’ll remain dedicated to the budget even if we’re saving less, if anything at all,” Drake said.

Financial Post

• Email: vferreira@postmedia.com | Twitter: VicF77